What is Leveraged Product?

Leveraged Products typically aim to deliver a daily return equivalent to a multiple of the underlying index return that they track. For example, if the underlying index rises by 10 percent on a given day, a two-time (2x) Leveraged Product aims to deliver a 20 per cent return on that day.

When index daily return rises 1%, product leveraged daily return rises 2%

+2%

What is Inverse Product?

Inverse Products typically aim to deliver the opposite of the daily return of the underlying index that they track. For example, if the underlying index rises by 10 per cent on a given day, a negative one-time (-1X) Inverse Product should incur a 10 per cent loss on that day.

When index daily return drops 1%, product daily return rises 1%

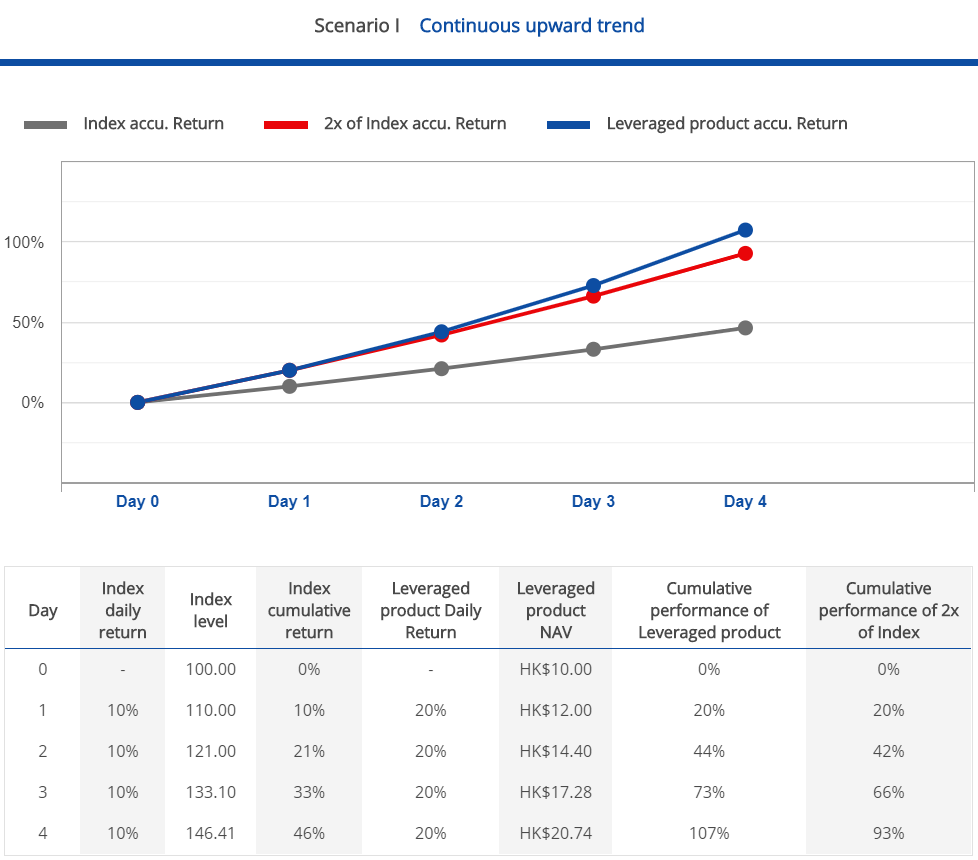

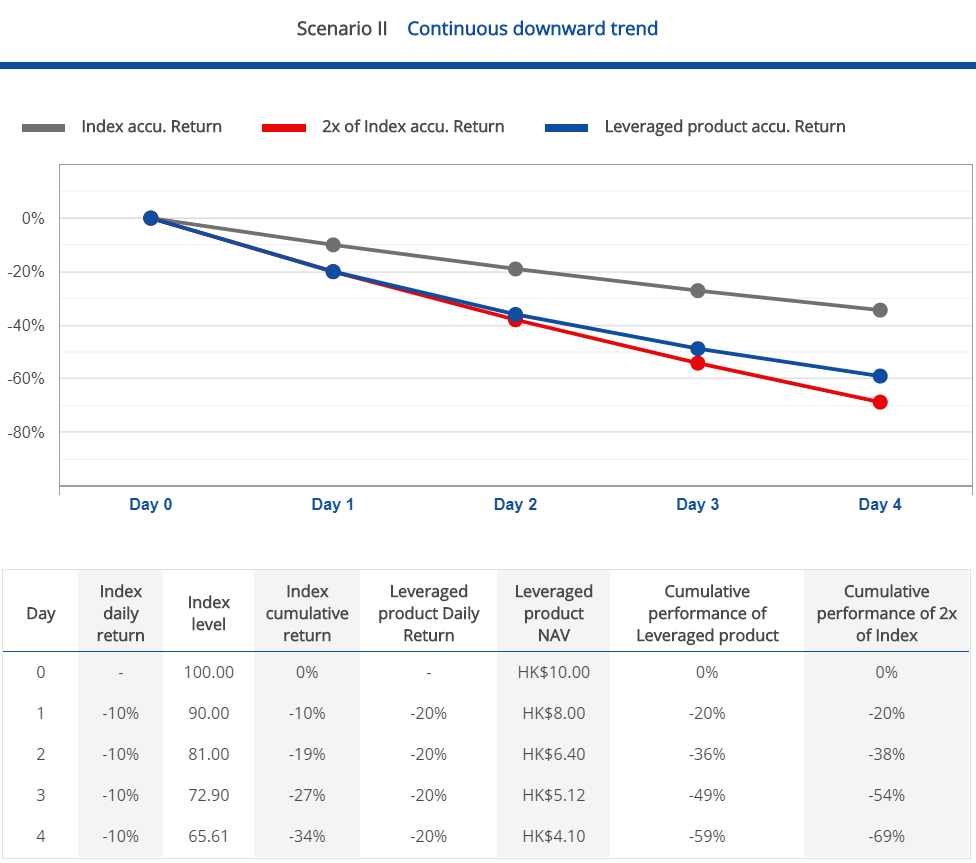

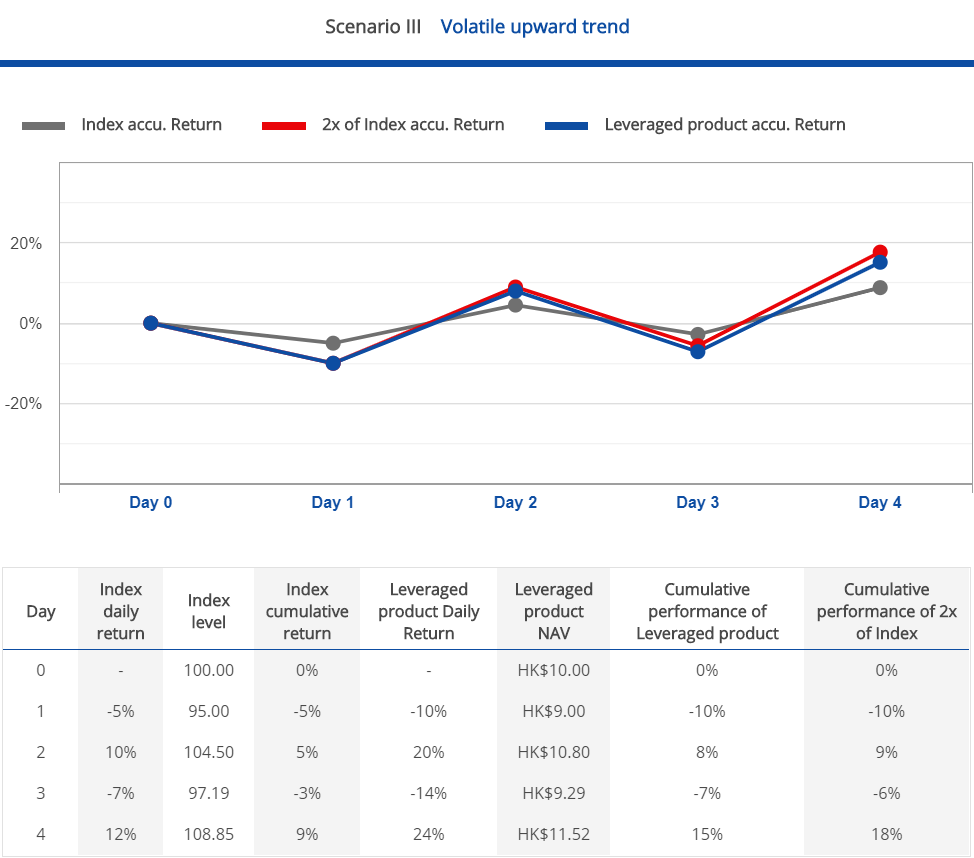

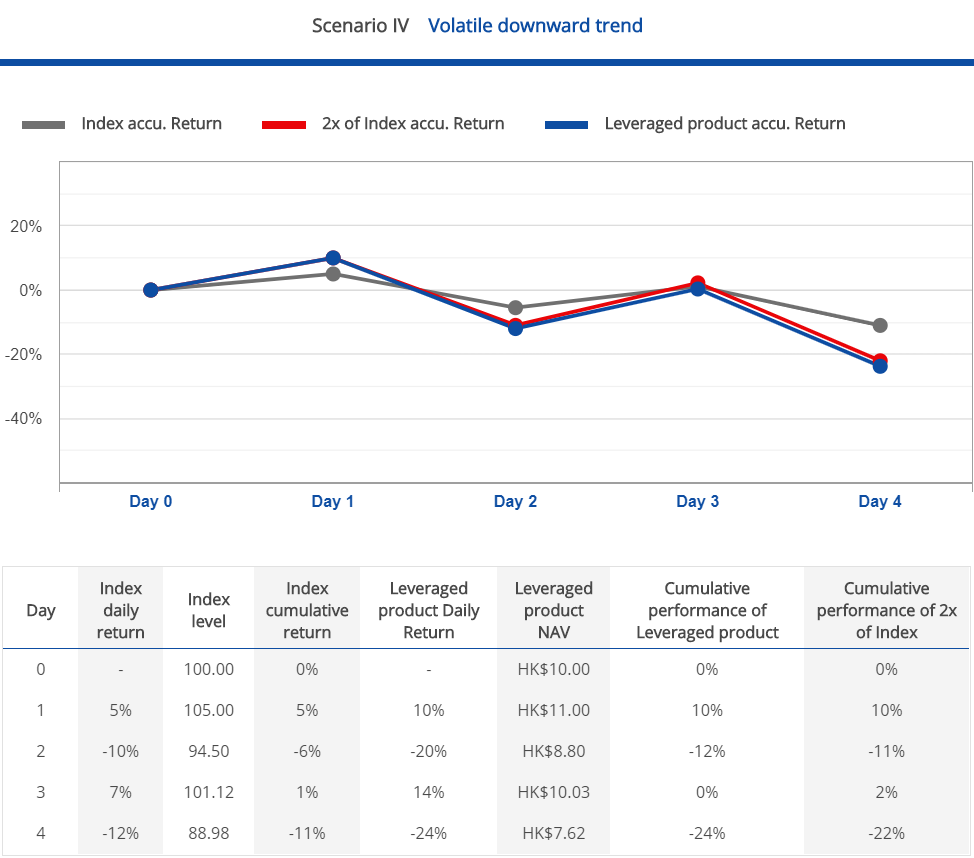

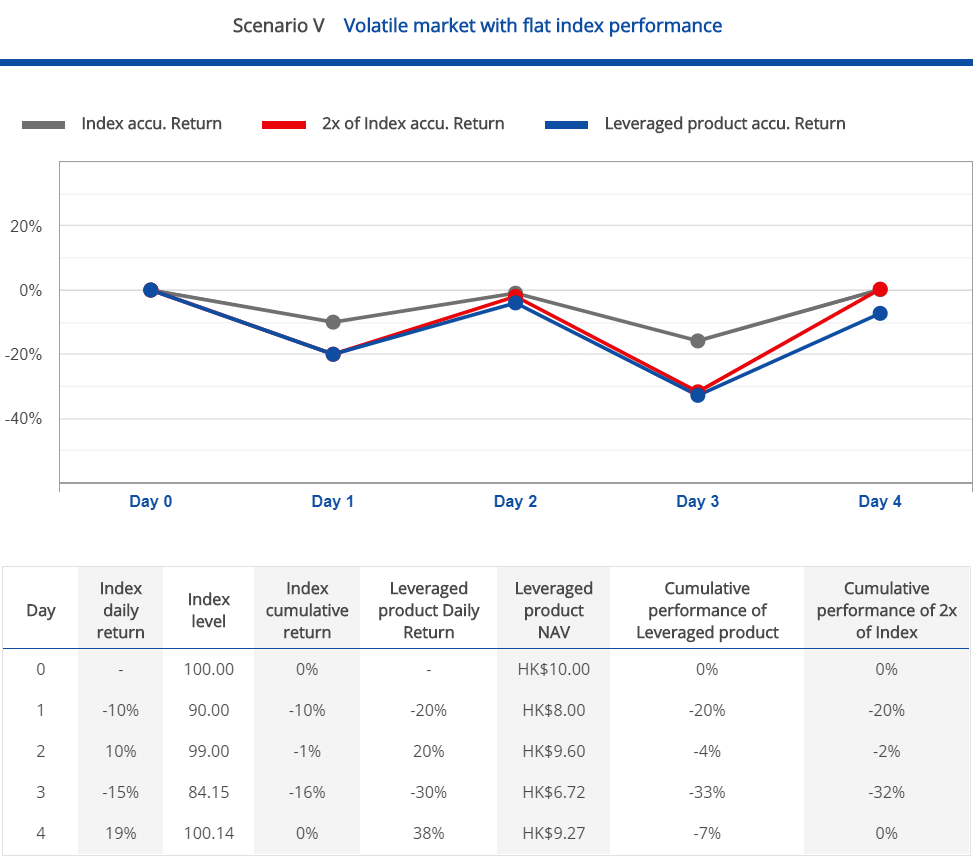

5 Case Study For Leveraged Product:

Comparison between the Index and the leveraged performance of the Index for a period longer than one day (i.e. comparison of the point-to-point performance).The Product‟s objective is to provide returns which are of a predetermined leverage factor (2x) of the daily performance of the Index. As such, the Product‟s performance may not track twice the cumulative Index return over a period greater than 1 Business Day. This means that the return of the Index over a period of time greater than a single day multiplied by 200% generally will not equal to the Product‟s performance over that same period. It is also expected that the Product will less than the return of 200% of the Index in a trendless or flat market. This is caused by compounding, which is the cumulative effect of previous earnings generating earning or losses in addition to the principal amount, and will be amplified by the volatility of the market and the holding period of the Product. In addition, the effects of volatility are magnified in the Product due to leverage. The following scenarios illustrate how the Product‟s performance may deviate from that of the cumulative Index return (2x) over a longer period of time in various market conditions. All the scenarios are based on a hypothetical $10 investment in the Product.

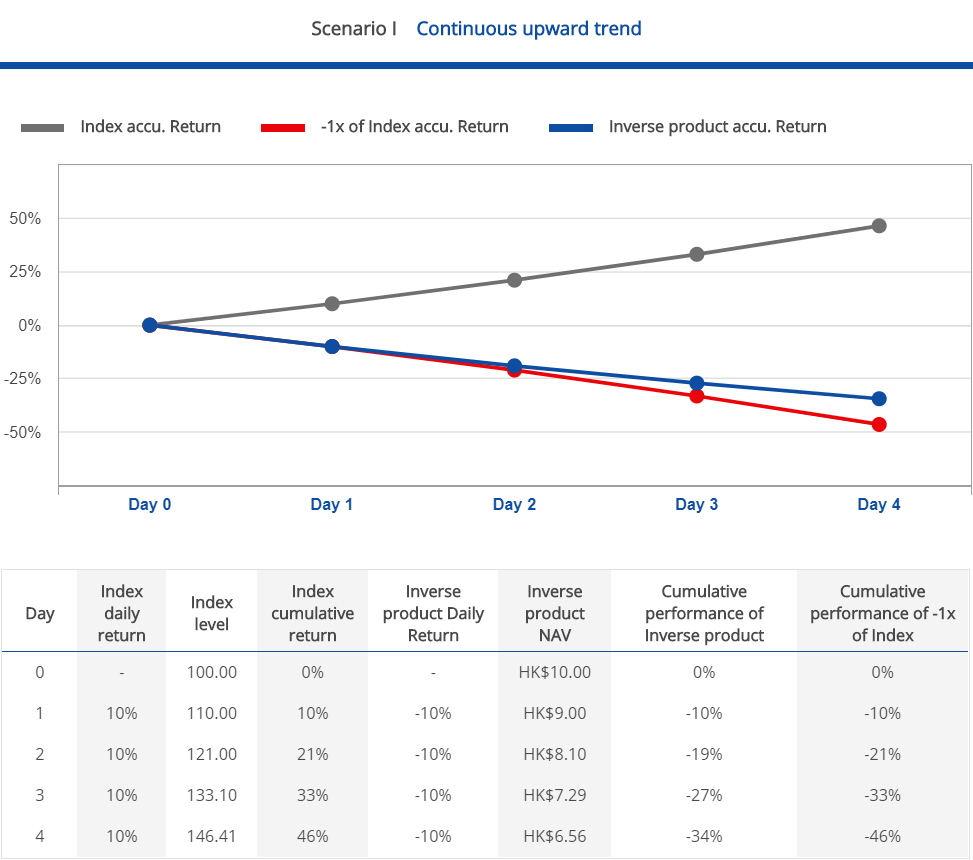

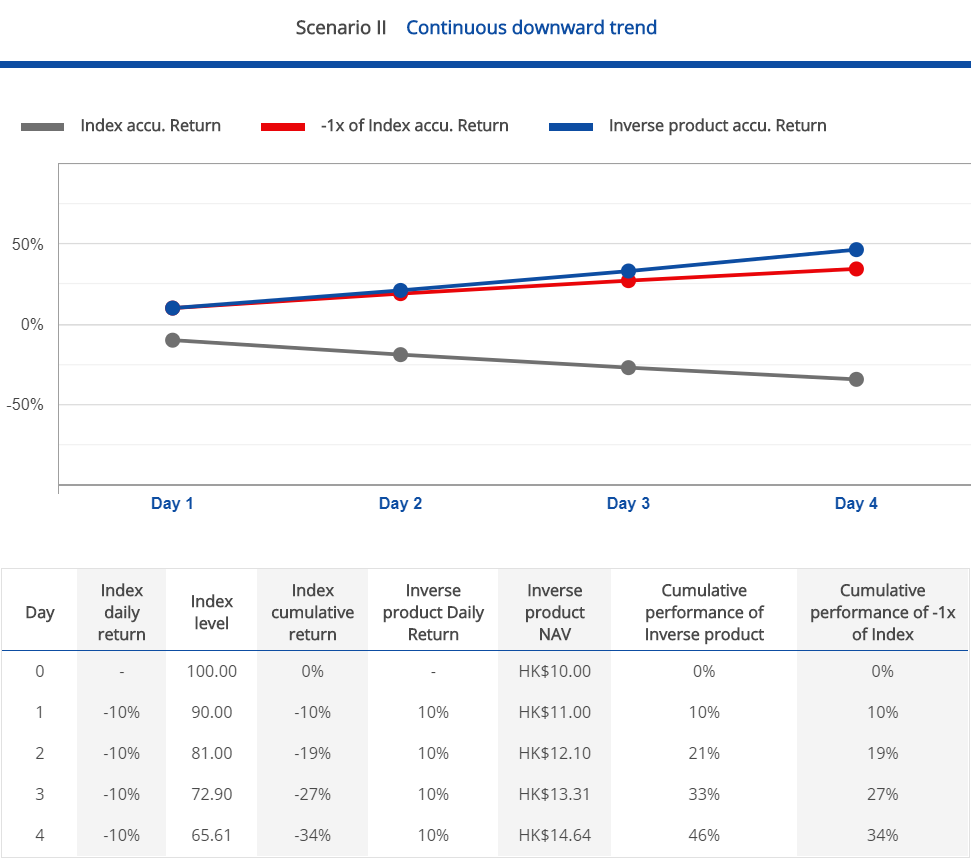

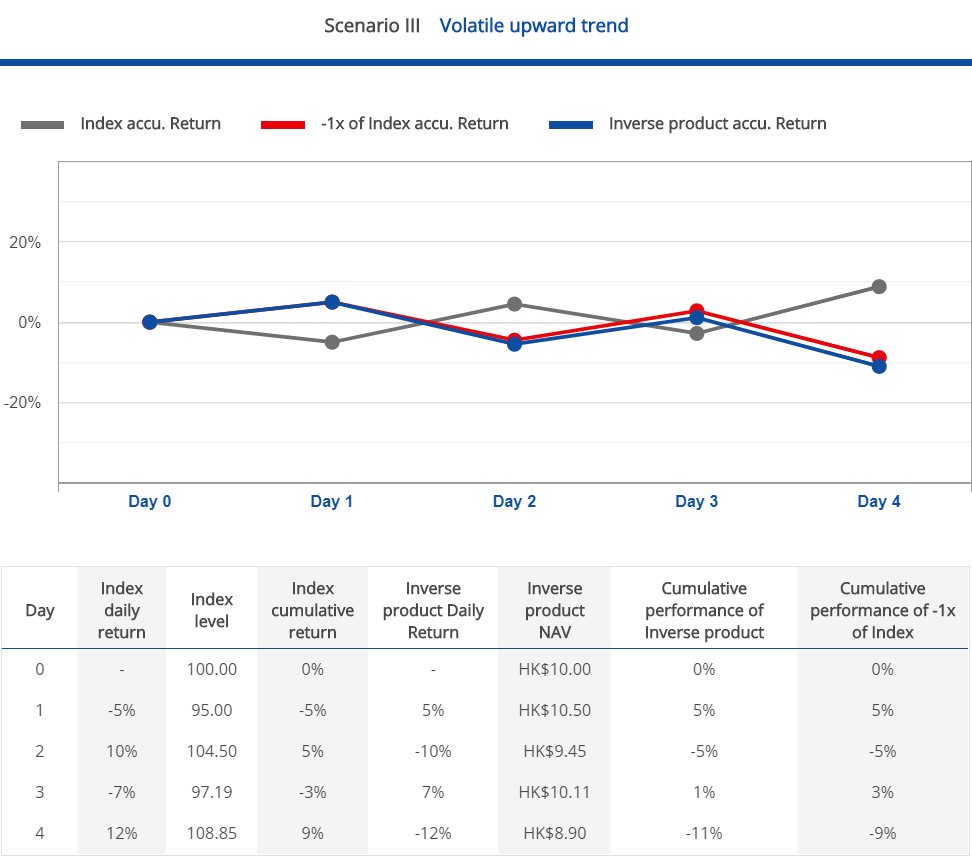

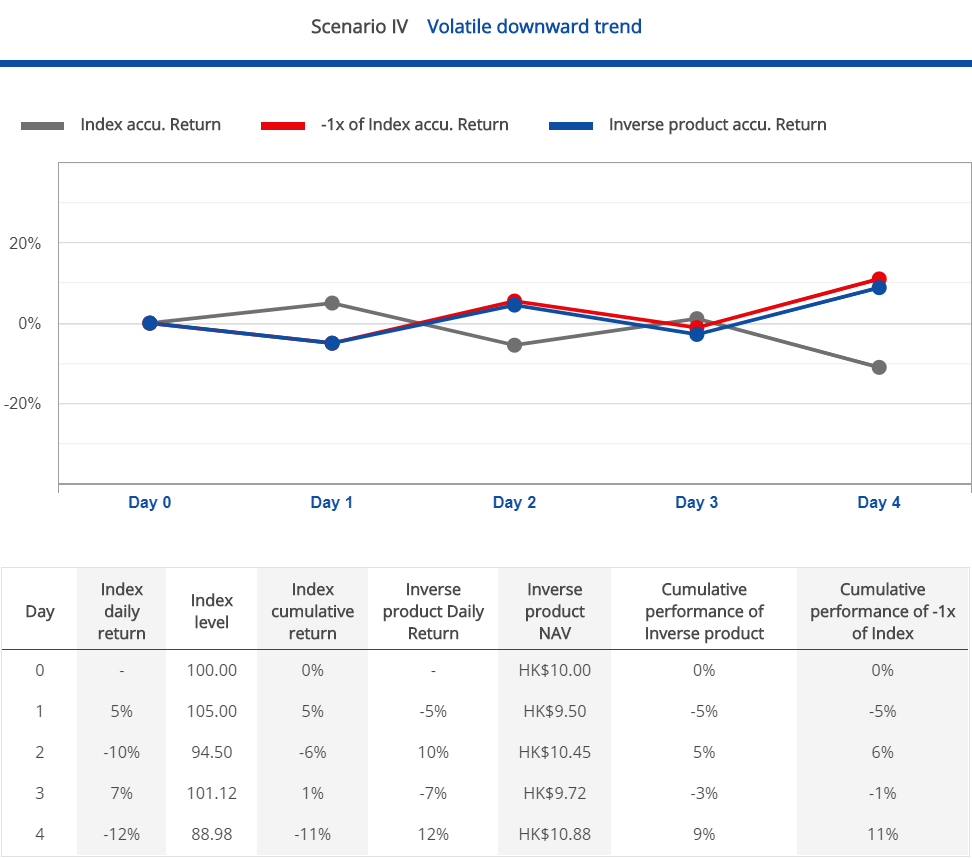

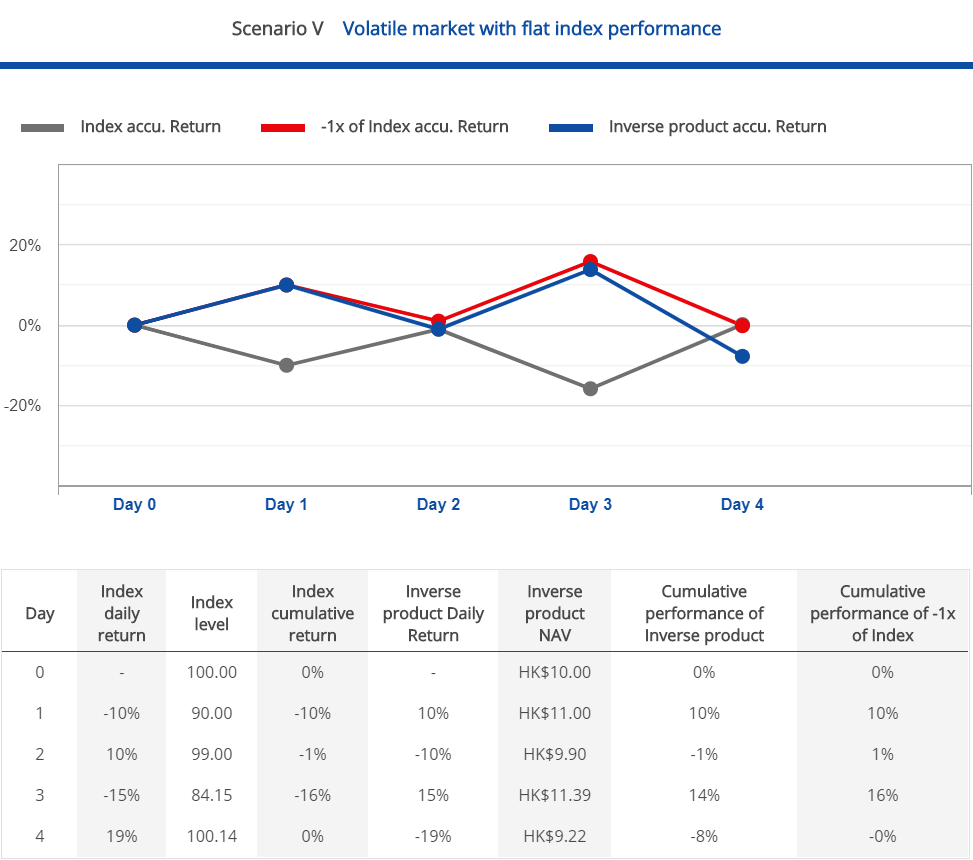

5 Case Study For Inverse Product:

Comparison between the Index and the inverse performance of the Index for a period longer than one day (i.e. comparison of the point-to-point performance). The Product‟s objective is to provide returns which are of a predetermined inverse factor (-1x) of the daily performance of the Index. As such, the Product‟s performance may not track -1x the cumulative Index return over a period greater than 1 Business Day. This means that the return of the Index over a period of time greater than a single day multiplied by -100% generally will not equal to the Product‟s performance over that same period. It is also expected that the Product will less than the return of -100% of the Index in a trendless or flat market. This is caused by compounding, which is the cumulative effect of previous earnings generating earning or losses in addition to the principal amount, and will be amplified by the volatility of the market and the holding period of the Product. The following scenarios illustrate how the Product‟s performance may deviate from that of the cumulative Index return (-1x) over a longer period of time in various market conditions. All the scenarios are based on a hypothetical $10 investment in the Product.